Office Address

Rukan Fatmawati Mas Blok 1 Kav.113 Lantai 4, Jakarta Selatan

Phone Number

082122285048

Email Address

sekretariat@akp2i.or.id

Rukan Fatmawati Mas Blok 1 Kav.113 Lantai 4, Jakarta Selatan

082122285048

sekretariat@akp2i.or.id

by Heru Yulianto

by Heru Yulianto

Jakarta – It is undeniable that e-commerce has grown rapidly in recent years, requiring the government to regulate and impose taxes on online transactions to increase state revenue. In addition, the government also wants to ensure that online and offline businesses have the same tax obligations, so that there is no discrimination between the two types of businesses.

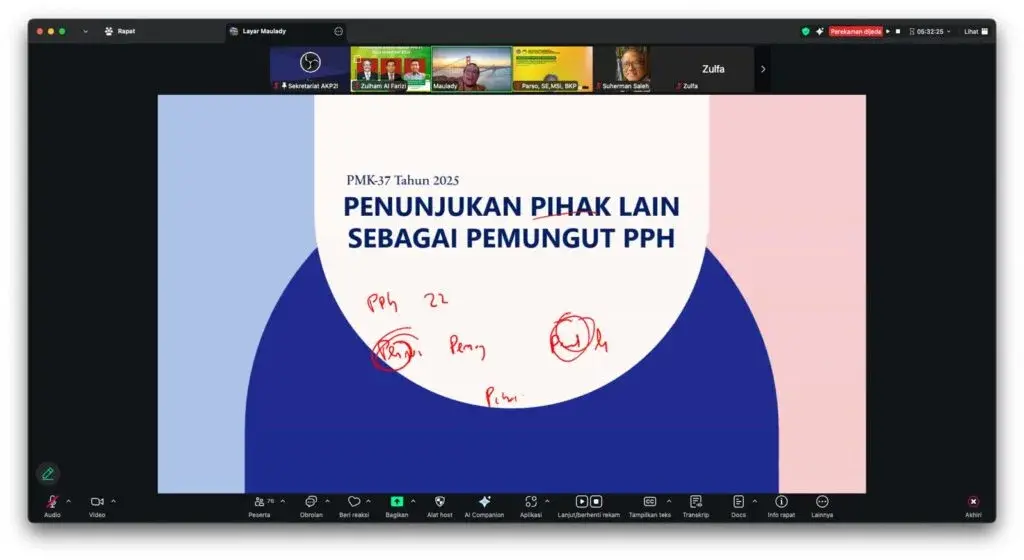

To support this, the Indonesian Public Tax Consultants Association (AKP2I) once again held a sharing session or tax seminar on Minister of Finance Regulation (PMK) Number 37 of 2025 concerning the Appointment of Other Parties as Income Tax Collectors (PPh).

In his speech, AKP2I Chairman Suherman Saleh said that this seminar was one of the association's efforts to support the government in disseminating information about the latest regulations, particularly those related to e-commerce.

“Given its important role in society, a more comprehensive understanding of e-commerce taxation is needed, particularly in relation to PMK No. 37 of 2025,” he said on Saturday (24/07).

He added that with the sharing session on e-commerce, it is hoped that consultants under AKP2I can gain more insight, knowledge, experience, and information more quickly and accurately.

“Hopefully, the information related to PMK Number 37 of 2025 on e-commerce will be useful for us and, more importantly, for others,” he added.

Appearing as a guest speaker, Tax Practitioner from the Directorate General of Taxes (DJP) Maulady Munandar said that the PMK stipulates that other parties appointed by the minister as collectors of Income Tax Article 22 are responsible for collecting, depositing, and reporting taxes on income received or earned by domestic traders.

“So, it is other parties who will collect the tax. These other parties conduct their trade through the Electronic Trading System (PMSE). Examples include Tokopedia, Shopee, Lazada, and others,” he said.

Furthermore, he said that the tax in the PMK is not a new type of tax.

“This is still Income Tax (PPh) 22 for those who collect and those who are deducted. This is part of the Personal Income Tax (OP) credit, and even part of the Final Income Tax credit for certain Final Income Taxes. So, it is not a new type of tax. However, the method of collection is simpler and easier,” he said.

In addition, Maulady also explained that perhaps taxpayers have been less compliant or there has been no collection by other parties. Therefore, there must be third-party collection to fulfill the principles of legal certainty, fairness, convenience, and administrative simplicity.

“Therefore, this is part of ensuring that our taxpayers implement the self-assessment system. So, this is also part of the supervisory task, from previously non-compliant to compliant, and ultimately, the payment of these taxes will help in the development of our country,” he said.